Earned Value Calculation is done by comparing the planned budget and scheduled work of a project to the actual costs incurred and work completed as the project progresses. Earned Value (EV) estimation provides valuable insight as to whether the project is on time and within budget.

Earned value calculations are the foundational metrics of Earned Value Analysis (EVA). EVA is crucial to accurately measuring current project performance and forecasting their results.

Most companies do not do EVA or they do it infrequently simply because it is too difficult to consolidate and manipulate the data required to do the calculation. Learn more about how Project Automation creates a fully integrated and automated Earned Value Management System.

To do an earned value calculation you must choose a method or rule for how progress will be tracked and measured. We call these “earning principles”. I will focus on three common earning principles in this article, what they are, how they are computed and why and when to use them.

Estimate at Completion Earned Value Calculation

Estimate at Completion (EAC) is the most versatile and frequently used earned value principle. EAC Includes all project budget positions, including labor, materials, equipment and expenses.

EAC is calculated by adding actual costs to the estimate to complete (ETC). EAC can be established on an ongoing basis as task owners report their actual costs and then estimate how much work/costs are required to complete their tasks.

Earned Value is then calculated based on actual costs out of Estimate at Completion (i.e. cost incurred to date out of expected cost at project completion).

Here is an example using EAC:

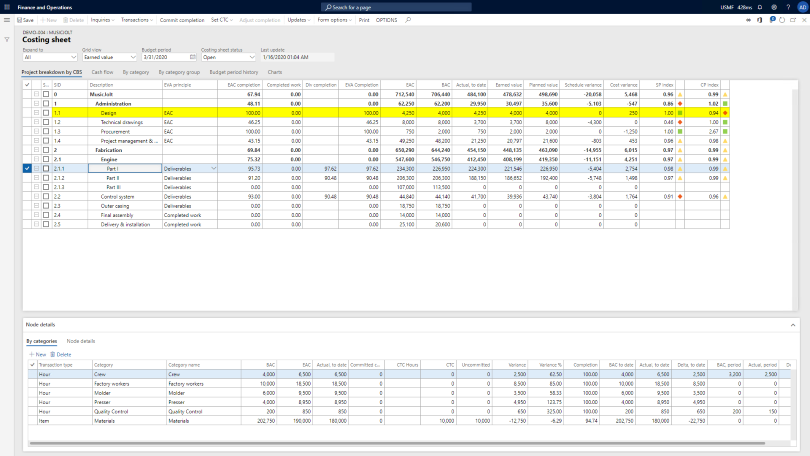

If we look at the highlighted line in this costing sheet we see that line 1.1 Design is using the EAC EVA principle. We can see that the EAC completion column says that the task is complete (100%), so the earned value is 100% earned as well (EVA Completion). In the Actual to date column we see that $4,250 was spent on this task, while the budget (BAC) and Planned value were $4000. Therefore, we had a Cost variance of $250. Then if you look at the Schedule Performance Index we completed the work on time, but the Cost Performance Index shows that we were over budget.

Here is another example:

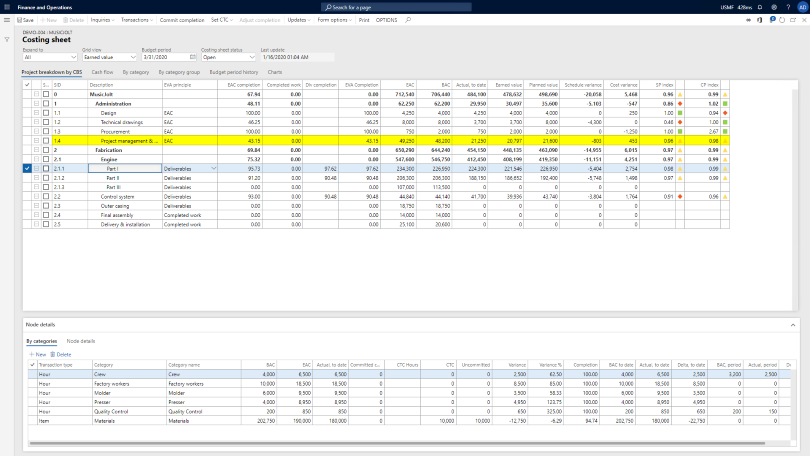

If we look at line 1.4 we can see that EAC and EVA completion are at 43.15% with Actual costs being $21,250. Our budget (BAC) for this task is $48,200 total, and at this point in the schedule our Planned value is $21,600. However, our EAC says now we are going to spend $49,250 on this task and we are only 43.15% complete, which means our earned value is $20,797. As a result, we can see our Schedule variance says we are behind schedule and our Cost variance tells us we are over budget.

EAC is the simplest principle to use as the value is automatically generated as part of the month-end (reforecasting) process.

Deliverables

Using Deliverables to calculate earned value is based on deliverables reported as completed out of total budgeted deliverables. The method requires you to enter quantity budgets against your Cost Breakdown Structure (CBS).

For example, a deliverable might be to install 1000 feet of piping. If 100 feet of piping has been installed, completion is calculated at 10%. This method is commonly used as progress tracking in construction industries. It is sometimes called “quantity reporting” or “production units”.

Here is a Deliverables example:

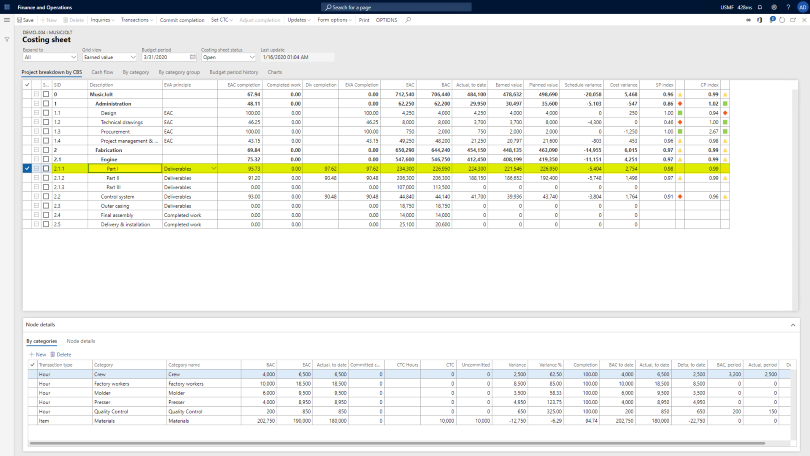

If we look at the highlighted row 2.1.1 we can see it is using the Deliverables EVA principle. The Div completion column tells us we are 97.62% complete on this task. Turned into dollars, we see that our Actual cost to date is $224,300. At 97.62% complete, we should have spent only $221,546 (Earned value). Additionally, at this point the task should be completed and total Planed Value is $226,950. If we look at the variance columns, we can see that we are both behind schedule and over budget on this task.

Completed Work

The Completed Work earning principle is based on actual work out of remaining work + actual work (measured in hours). In basic terms, it is the hours spent to date out of expected hours required in total at task/project completion.

For example, 100 hours are required for task X over a period of 4 weeks. At 2 weeks 30 hours were completed while 70 remain, 30% of the work is done while the planned completion rate was 50%. Assuming hours = cost, we are behind schedule. If a new estimate of 80 hours would be required to complete the task, then we are 10 hours over budget as well.

Completed Work earned value calculations are typically used in labor intensive fields. Professional Services companies tend to use this principle when computing earned value.

Earned Value Management

Most companies do not do EVA or they do it infrequently simply because it is too difficult to consolidate and manipulate the data required to do the calculation. That is unfortunate because it is a powerful tool for meaningfully understand the state of your projects and thereby your business.

The key to making EVA a regular part of your routine is to integrate all your data into one Earned Value Management System. That means that your processes and workflows are managed in that system as well. When that happens, EVA can be done automatically.

Project Automation provides that fully integrated, comprehensive business system for project-based companies.

Evaluate Any ERP or Business System for its Project Business Capabilities

Resource Management: Microsoft Dynamics 365 vs. PlanAutomate

Henrik Lerkenfeld

Henrik is a driving force behind the product success of the PlanAutomate solution, bringing a systematic approach to process design and a deep understanding of project-based industries. His work focuses on natively unifying critical project data and processes, including financials, operations, and supply chain, into a single source of truth for project-driven organizations inside Dynamics 365 Finance. His experience spans decades of working with Microsoft ERP systems for project-centric companies. He also leads the services team at Adeaca that implements the Dynamics 365 Finance, Supply Chain Management, and PlanAutomate.

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.